A Spanish VAT number is your tax ID (NIF) with "ES" added in front, once your business is approved for intra-EU trade. The CIF you sometimes see on old paperwork is the same number under an older label.

The NIF (Número de Identificación Fiscal) is your tax ID. Every company, freelancer and resident doing anything official has one. For domestic invoices, the NIF is all you need. When you start billing EU clients, that same number gets an "ES" prefix and becomes your intra-community VAT number, but only once your registration is complete, not automatically.

The CIF (Código de Identificación Fiscal) was the old tax ID for legal entities like SLs and branches. It was officially merged into the NIF in 2008. It's legally obsolete, but banks, suppliers and government forms still ask for "CIF" out of habit. If someone asks you for your CIF, give them your NIF, it's the same number.

A Spanish NIF is 9 characters: a letter or digit, 7 digits in the middle, and a check character. The first character tells you what kind of holder it is, an individual, an SL, a public body, and so on. The intra-community VAT number is just that same NIF with "ES" added as a prefix.

Having a NIF does not mean you can issue invoices to EU clients without charging Spanish VAT. To trade B2B across EU borders without adding local VAT, you need to be registered in the ROI (Registro de Operadores Intracomunitarios). Without that registration, your NIF is domestic-only, no matter who your client is.

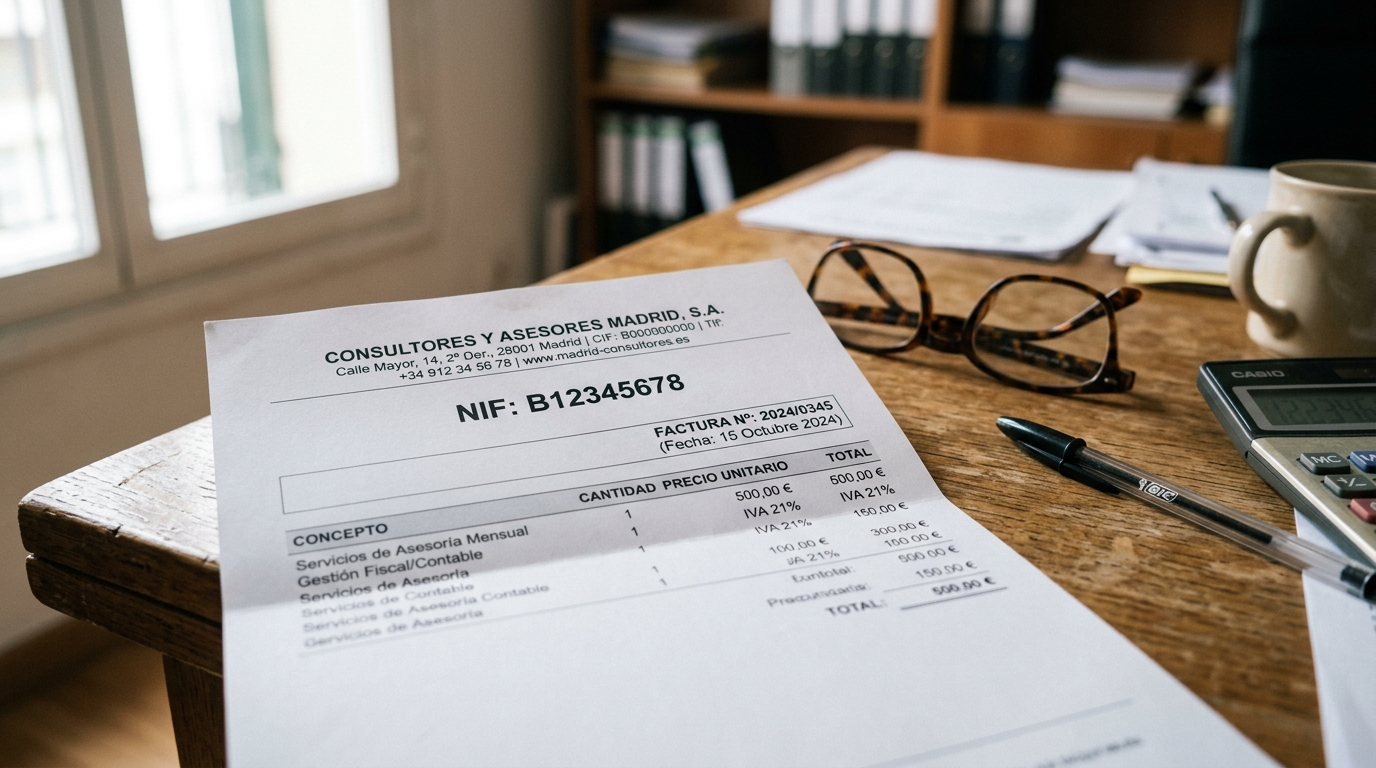

You run an SL in Madrid that builds websites. Your NIF: B12345678. A client in Berlin hires you for a €10,000 project.

If your SL is registered in the ROI, you invoice the German client for €10,000 with no Spanish VAT added. The invoice shows your intra-community VAT number (ES B12345678) and the client's, plus the note "inversión del sujeto pasivo" (reverse charge), the client accounts for the VAT on their end in Germany, not you in Spain. You then report the operation in Modelo 349, the periodic recap of intra-community transactions, alongside your normal Modelo 303.

If your SL is not registered in the ROI, you can't apply the reverse charge, even though the client is abroad. In practice, most SLs register in the ROI as soon as they expect a single EU client, fixing an invoice after the fact is far more painful than registering upfront.

Same NIF, same business, two different invoices, and the only difference is whether that ROI registration happened first.

For most freelancers, the NIF arrives automatically as part of the freelancer registration process, no separate application. For companies, you submit Modelo 036 to the AEAT as part of registering the company, and get a provisional NIF within days, with the definitive one issued about a week later.

If you expect to invoice EU clients, request ROI registration on the same Modelo 036 rather than adding it later. Approval typically takes four to six weeks.

Two free official tools do this:

If a number doesn't show up in VIES, it doesn't mean the business is invalid. It means they haven't activated intra-community VAT, and they need to before billing you cross-border.

Colloquially, yes. Legally, no. The 2008 merger made the CIF and NIF identical.

Yes. For foreigners with a Spanish NIE, the NIE acts as the NIF for all tax purposes.

You need a NIF to operate at all. You only need intra-community VAT registration (the ROI) if you invoice clients elsewhere in the EU B2B.

The NIF is your domestic tax ID. The intra-community VAT number is the same NIF with "ES" added as a prefix, active only once you're registered in the ROI.

No. Unlike many EU countries, Spain has no minimum revenue threshold for VAT registration.

Provisional NIFs arrive within days, definitive ones follow within about a week. ROI registration for intra-community VAT typically takes four to six weeks.